Combinatorial Purged CV (CPCV)¶

This implementation is based on Chapter 12 of the book Advances in Financial Machine Learning.

Given a number φ of backtest paths targeted by the researcher, CPCV generates the precise number of combinations of training/testing sets needed to generate those paths, while purging training observations that contain leaked information.

CPCV can be used for both for cross-validation and backtesting. Instead of backtesting using single path, the researcher may use CPCV to generate various train/test splits resulting in various paths.

CPCV algorithm:

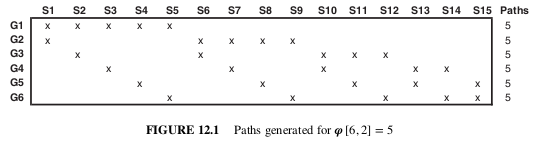

Partition T observations into N groups without shuffling, where groups n = 1, … , N − 1 are of size [T∕N], and the Nth group is of size T − [T∕N] (N − 1).

Compute all possible training/testing splits, where for each split N − k groups constitute the training set and k groups constitute the testing set.

For any pair of labels (y_i , y_j), where y_i belongs to the training set and y j belongs to the testing set, apply the PurgedKFold class to purge y_i if y_i spans over a period used to determine label y j . This class will also apply an embargo, should some testing samples predate some training samples.

Fit classifiers ( N ) on the N−k training sets, and produce forecasts on the respective N−k testing sets.

Compute the φ [N, k] backtest paths. You can calculate one Sharpe ratio from each path, and from that derive the empirical distribution of the strategy’s Sharpe ratio (rather than a single Sharpe ratio, like WF or CV).

When combinatorial splits were generated, CombinatorialPurgedKFold class contains backtest paths formed from train/test splits.

Image showing splits for CPCV(6,2)¶

Presentation Slides¶

Note

These slides are a collection of lectures so you need to do a bit of scrolling to find the correct sections.

pg 14-18: CV in Finance

pg 30-34: Hyper-parameter Tuning with CV

pg 122-126: Cross-Validation